Your super contributions just went up

KEY POINTS

- Your employer now contributes the equivalent of 11% of your salary to your super.

- Over time this extra 0.5% equates to a solid boost to your super.

- It’s a good time for some super housekeeping: reviewing insurance, contributions etc.

- The increase particularly benefits lower-income earners.

The contributions your employer makes to your superannuation account increased on July 1. They’re now equal to 11% of your salary, a jump of 0.5% from the past financial year.

That is now the minimum amount your employer must pay into your fund on your behalf (this is called the super guarantee). If your super contributions are listed on your payslip, you should see the increase there from the July 2023 pay period.

“Another 0.5% increase is scheduled for July 2024 and the following year. It’s going to add up to a substantial increase in the money you have to fund your life after work,” explains smartMonday head smartCoach Matt Davey.

“That increased amount in your super will achieve greater results due to compound returns – where the gains of each year are further built on in following years.”

Even taking into account periods of poor performance, such as calendar year 2022, returns even out over time, such as smartMonday’s Growth – Index investment option, achieving an average 8% annual return for the past 10 years (as at the end of May 2023).

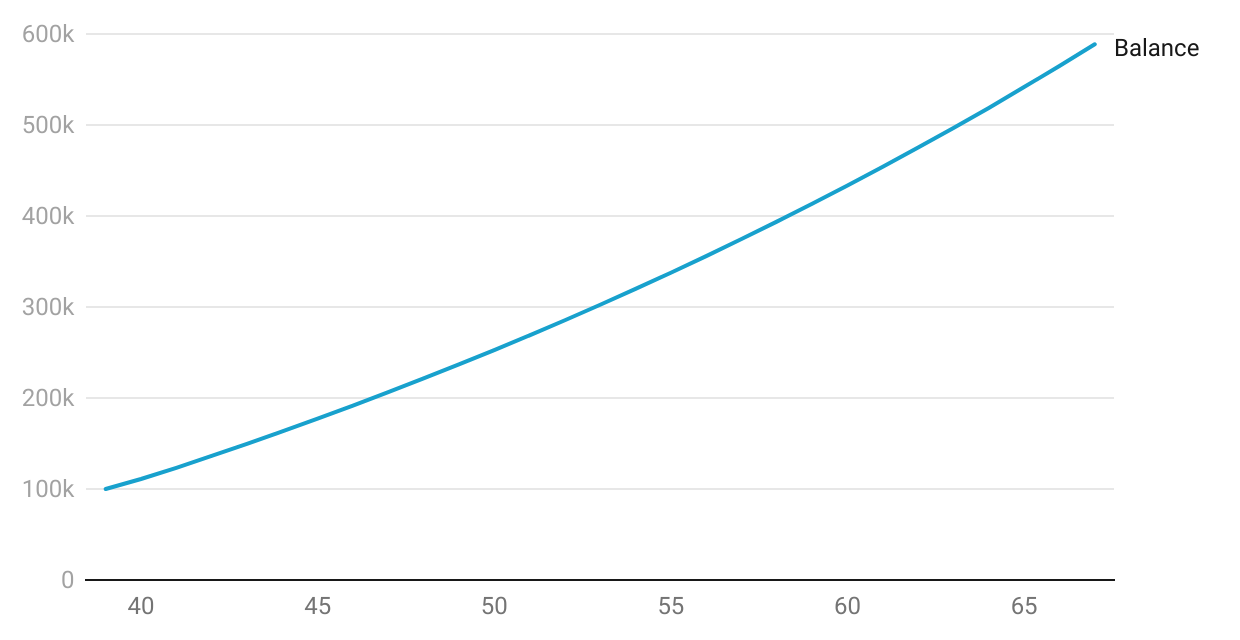

The below graph shows the effect of compound returns at the increased contribution rate of 11% on a super balance of $100,000 for a 40-year-old member.

Super balance based on 11% contribution rate

Check in with your super

It’s a new financial year, bringing with it a permanent increase to your super contributions.

“This makes it a perfect time to do a quick review of your superannuation, including the investment you have, if your insurance is right and a few other essential matters such as additional contributions,” says Davey.

Log in to your personal homepage and run through this quick housekeeping checklist:

Review the performance of your investment option (keeping in mind that 2022 was not a good year for almost any investor, so focusing on the long term is usually best).

Decide if you're insured for the right amount.

Nominate a beneficiary, so you control who will get your super.

Making additional contributions could benefit your super in the long term. Consider if they're right for you.

An outsized impact for lower earners

“The increase in the super guarantee will be particularly advantageous for those who traditionally receive little or no super. These are part time and casual workers, which often means younger people and women,” says Davey.

Looking ahead to the impact of the full 12% super guarantee rate to take effect by 2025, Australian Treasurer Jim Chalmers said in a statement on July 1 last year that for total super balance “it will deliver an extra $76,000 to the typical Australian worker in retirement”.

Tax issues for higher earners

Contributions to super are limited to $27,500 a year at the concessional tax rate of 15%. (This may be higher if you’ve contributed below that limit in recent years under what is known as ‘carry forward arrangements’.)

If you contribute more than the concessional cap then your excess contributions will be added to your tax-assessable income for that year.

“People close to their concessional contributions cap will need to carefully assess the impact of their increased super guarantee payment, particularly if it may push their contributions over that cap,” explains Davey.

If you are currently sacrificing some of your salary to make extra super contributions, you should also consider if the increased employer contributions mean those arrangements should be changed.

Some of the issues raised above can be complex, so consider obtaining qualified financial advice or speaking with a smartMonday smartCoach.

Any questions? Speak to one of our smartCoaches

- live chat: smartMonday.com.au

- email: smartcoach@smartmonday.com.au

- phone: 1300 262 241