smartMonday Performance: July-Sept 2024

We’re into the first quarter of the 2025 financial year, which runs from July through September. Here’s everything you need to know about your smartMonday fund’s performance in the three months to 30 September.

The big picture

Global markets were volatile early in the quarter as share markets came under pressure after the Bank of Japan’s rate hike surprised investors and weak US labour market data raised fears of a faster slowdown than had initially been anticipated.

By September, two significant events helped turn things around. Firstly, the US Federal Reserve (Fed) cut interest rates more than expected, which gave investors confidence that the battle against inflation is nearing an end. The US election result could shift the investment landscape, but it isn’t a reliable predictor of investment performance. We believe the prudent approach is to prepare for different economic scenarios as new policies are implemented.

Secondly, China launched larger-than-expected economic stimulus – its most significant since 2015 – to support its weakening economy. These measures worked; the last three weeks of September saw a remarkable 31% rally in the Hang Seng index, transforming it from one of the poorest performers of the past year to a top 3 market leader. These surges can yield great returns – but China’s economy still faces significant challenges, including falling property and consumer prices, so it’ll need to do a bit more to shore itself up.

The story in Australia

The Reserve Bank of Australia (RBA) continues to steer towards a balanced approach to interest rates, trying to address inflation without causing more unemployment. This comparatively conservative strategy is trying to mitigate the cost-of-living pressure on Australians. Despite positives for the employment market, inflation in Australia is falling more slowly than in other countries, which has delayed any potential rate cuts.

Australia’s strong labour market and comparatively stable economic environment may increase demand for local bonds, particularly from international investors. Bonds make up the more stable, defensive part of your superannuation portfolio.

Return to office drives Aussie growth; while fossil fuels drag

Recent moves by companies to require their staff to return to offices has driven growth in real estate. This benefited Aussie companies like Charter Hall, which manages real estate investment across office, retail and social infrastructure.

It was more bad news for the fossil fuel energy industry. Australian petroleum firm Woodside and natural gas supplier and exporter Santos didn’t perform well, continuing fossil fuel’s long-term drag on investment markets.

Bond yields fluctuate under policy shifts

Bond markets in Australia and globally have been fluctuating recently, underscoring a period of heightened volatility driven by economic data releases and central bank policies. Softer US data led to expectations of monetary easing by the Fed, which drove investors toward the safety of US Treasuries, pushing yields down. The Fed's unexpected aggressive rate cut in September suggests it’s concerned about economic growth. This caused an initial rally in bond markets before communications issued by the Fed tempered future rate cut expectations.

Australia’s bond market was also influenced by central bank actions and domestic economic indicators. Yields dropped initially, because of weaker than expected inflation. But the surprisingly strong employment figures helped save the day, combined with the RBA’s stance against rate hikes. All of this shows that bond markets are pretty sensitive to economic data and messages from central banks.

Recession fears melting away?

Compared to the first six months of 2024, by September we were seeing solid performance from a wider range of companies and increasing expectations for rate cuts in 2024. While the Magnificent Seven tech stocks (Alphabet/Google, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) continued to deliver impressive returns, the gap in earnings between tech stocks and other US listed companies has narrowed. Markets are starting to relax, expecting an economic soft landing, and the Fed pushing down interest rates has the market now looking for around a 1% rate cut by the end of the year.

This feeling benefited rate-sensitive asset classes during the quarter, including property, infrastructure, and bonds. The Australian share market also delivered strong performance, predominantly driven by the banking and finance sector, as recession fears waned.

A super strong September

Superannuation returns continued to defy expectations amid market volatility in a typically subdued time of year, with the median balanced option returning 1.2% in September and 3.7% for the quarter. Despite the positive start to the financial year a backdrop of uncertainty remains that could impact future returns. Global tensions, the outcome of the US presidential election and an unclear interest rate path in Australia contribute to this uncertain landscape.

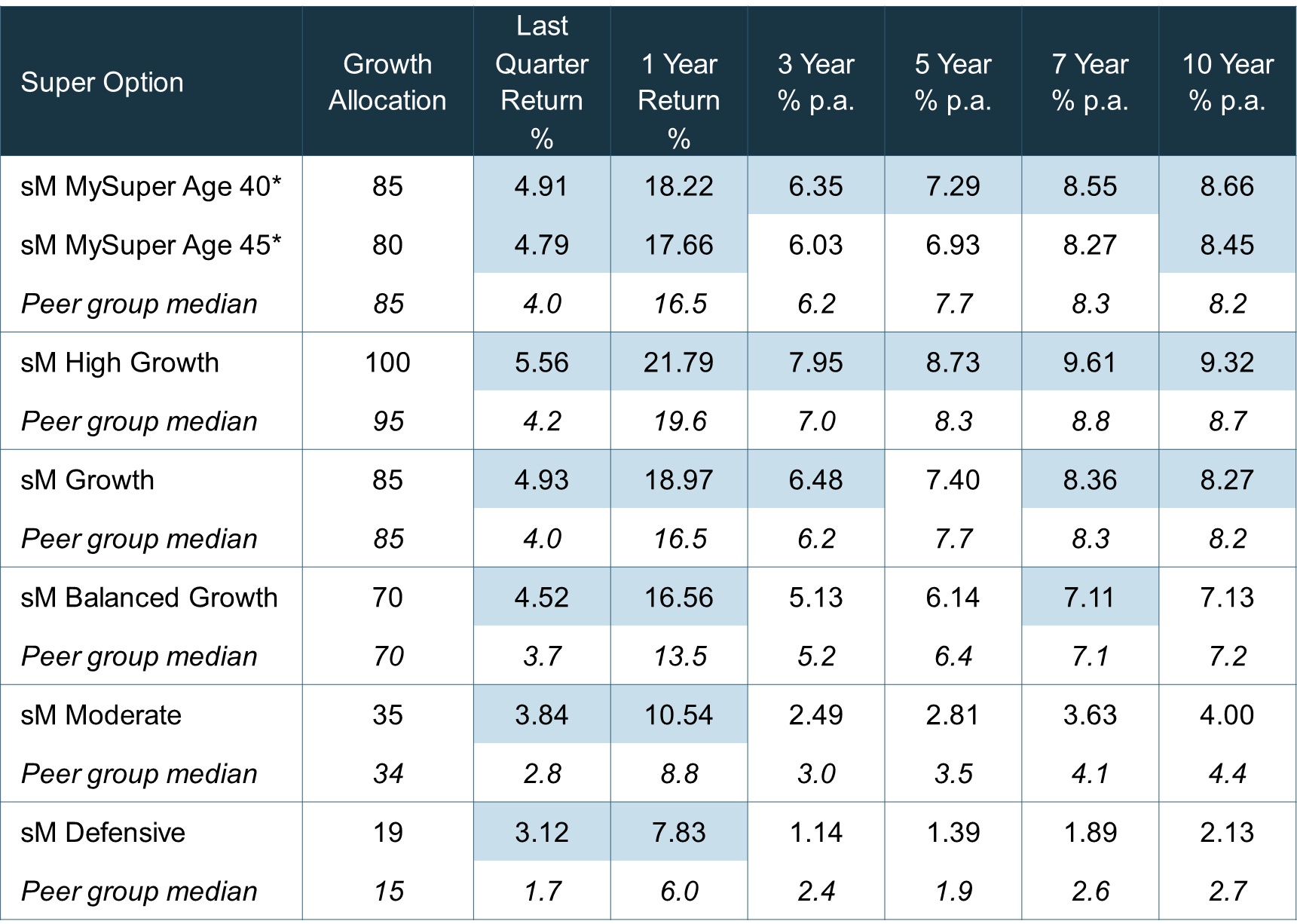

smartMonday’s options posted strong gains in the September quarter, as global and Australian shares continued to perform well over the period.

From 1 July to 30 September 2024, the largest cohort of MySuper members (age 40-45) returned between 4.8%–4.9%, High Growth and Growth focused options returned 5.6% and 4.9% respectively, while the Balanced option returned 4.5%.

In the table below, shading shows where smartMonday has outperformed the SuperRatings median.

Looking forward

Trump’s return to the White House comes at a time of record highs for the property and share market. Although Trump has promised to lower inflation, his policies – including cutting taxes, imposing widespread trade tariffs and deporting migrant workers – are considered inflationary. The Fed lowered interest rates slightly in the wake of the election, but now needs to strike a balance between keeping inflation in check without further weakening the job market as Trump’s pledges play out across the economy.

Globally, the greater risk remains if major economies were to soften more than expected. While this can relieve inflation, central banks will be vigilantly monitoring signs of employment and other economic metrics.

For the moment, we’re cautiously positive for alternative investments and are finding good returns in healthcare, housing and high-quality loans, which all help make up the more defensive foundation of your super.